Is your Bitcoin property or is it money? The answer depends entirely on who you ask and what they want to achieve. If you are filing taxes with the IRS, it is property. If you are trying to move funds across borders under banking laws, regulators might call it currency. This confusion isn't just a headache for accountants; it defines how you can own, transfer, and protect your wealth in the digital age.

For centuries, the law had a simple job: sort things into boxes. You either owned a piece of land (real property) or a movable object like a car or a stack of cash (personal property). But the rise of blockchain, a decentralized digital ledger technology that records transactions across many computers so that the record cannot be altered retroactively has shattered these neat categories. Today, understanding whether an asset is classified as property or currency determines your tax bill, your ability to use it as collateral, and even whether you can inherit it without a court fight.

The Traditional Divide: Real vs. Personal Property

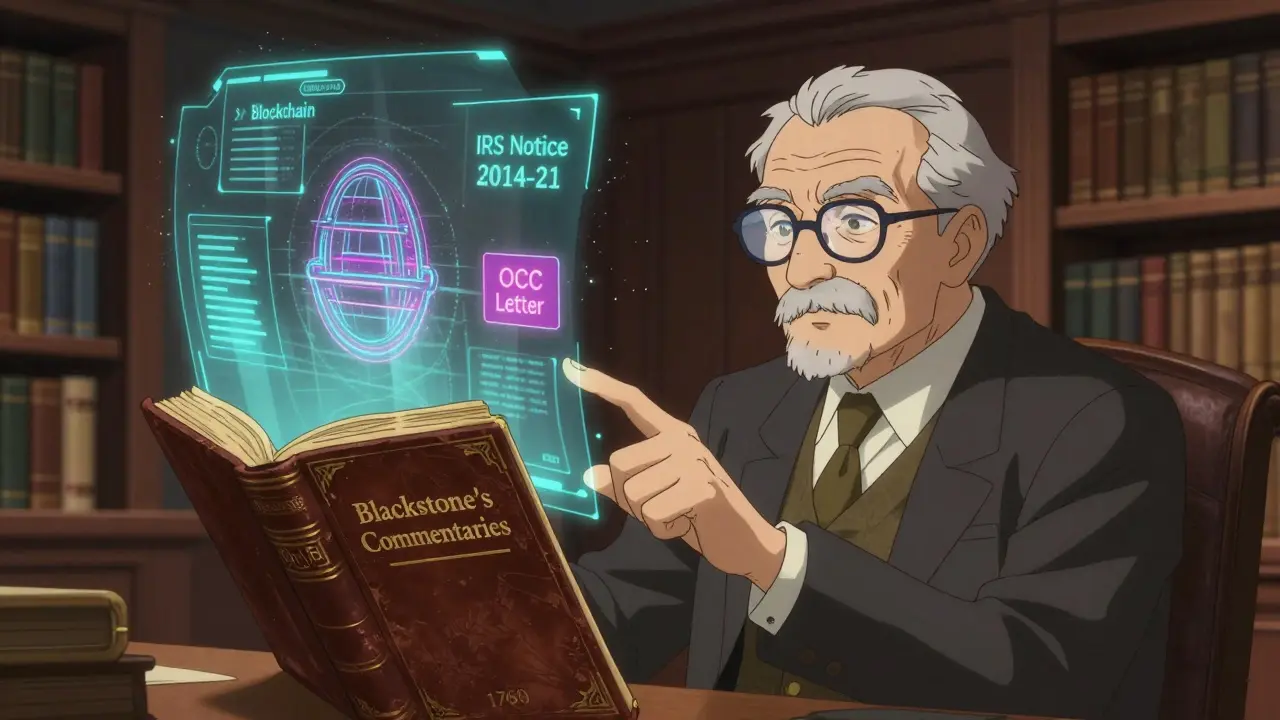

To understand why digital assets are so messy, we first need to look at how traditional law works. The foundation comes from English common law, specifically William Blackstone's 'Commentaries on the Laws of England' published in the 1760s. He established a clear split: real property (land and anything permanently attached to it) and personal property (everything else).

This distinction matters because the rules for transferring them are totally different. Selling a house requires a formal deed, title insurance, and recording fees that can run hundreds of dollars. It’s slow, expensive, and heavily regulated. Selling a chair? You hand it over, maybe sign a receipt, and you’re done. The law treats these differently because land is scarce and permanent, while chairs are not.

Within personal property, there is another split: tangible vs. intangible. Tangible property is physical stuff you can touch-coins, paper money, jewelry. Intangible property is a right or a claim-like a stock certificate or a bank balance. Here is where the trouble starts. When you hold a $100 bill, you hold tangible personal property. When that same value sits in your checking account, it becomes intangible property, legally known as a "chose in action." You don’t own the money itself; you own the bank’s promise to pay you.

Where Does Currency Fit In?

Currency is a weird hybrid. On one hand, physical coins and notes are tangible personal property. On the other hand, courts have long argued that money is not really "property" in the traditional sense because its primary purpose is to measure value, not to be held as an asset itself. In the 1925 case Webb v. United States, the Supreme Court noted that money used in business is the "measure of property," not property itself.

This philosophical debate has practical consequences. If money is just a medium of exchange, you generally don’t pay capital gains tax when you spend it. You only pay income tax when you earn it. But if something is classified as property, every time you trade it for something else-even for another cryptocurrency-you trigger a taxable event. This is the core of the current legal chaos surrounding digital assets.

| Asset Type | Legal Classification | Transfer Mechanism | Tax Implication (US) |

|---|---|---|---|

| Real Estate | Real Property | Deed & Registry | Capital Gains on Sale |

| Physical Cash | Tangible Personal Property | Physical Handover | No Tax on Spending |

| Bank Balance | Intangible Property (Chose in Action) | Electronic Transfer | Income Tax on Earnings |

| Bitcoin/Crypto | Contested (Property vs. Currency) | Blockchain Transaction | Capital Gains (IRS View) |

The Crypto Conundrum: Property or Money?

When Bitcoin emerged, lawyers were forced to fit a square peg into a round hole. In 2014, the Internal Revenue Service (IRS) issued Notice 2014-21, declaring that virtual currencies are treated as property, an asset that has economic value and can be owned, transferred, and taxed upon exchange. This means if you buy Bitcoin for $1,000 and later trade it for goods worth $1,500, you owe capital gains tax on the $500 profit. Even trading Bitcoin for Ethereum triggers a taxable event.

However, this doesn't align with how banks view these assets. The Office of the Comptroller of the Currency (OCC) issued Interpretive Letter 1179 in 2020, stating that banks can provide custodial services for cryptocurrencies, effectively treating them as currency for banking regulations. This creates a bizarre situation: the IRS says it’s property for taxes, but the OCC says it’s currency for banking compliance.

Why does this double standard matter? Because it affects how you handle disputes. If your crypto wallet is hacked, are you suing for conversion of property (like someone stealing your laptop)? Or are you dealing with a failed financial transaction (like a bank error)? The remedy changes based on the label. Courts are still sorting this out, leading to inconsistent rulings across different states.

Impact on Estate Planning and Divorce

The ambiguity hits hardest in life’s most stressful moments: death and divorce. According to reports from the American Academy of Estate Planning Attorneys, nearly half of probate cases involving digital assets require judicial clarification because the will didn't specify how to classify the crypto.

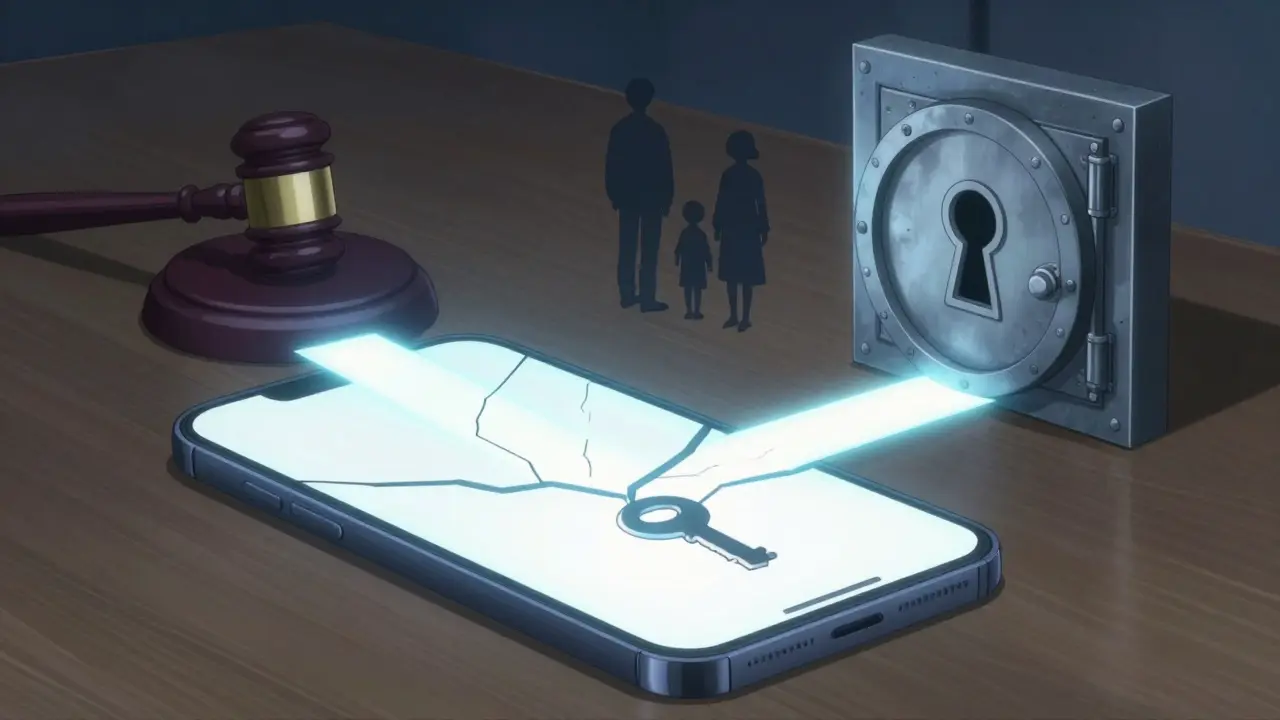

In estate settlements, physical jewelry is distributed immediately. Bank accounts often freeze for months. Crypto wallets? They exist in a gray zone. If the keys are lost, the "property" vanishes forever. If the heirs don’t know the password, they can’t access the "currency." Unlike a bank account, there is no customer service line to reset access. The legal classification determines whether the executor of the estate has the right to access private keys, which is a privacy nightmare for some families.

In divorce cases, the stakes are equally high. A 2022 survey by the American Academy of Matrimonial Lawyers found that 31% of high-net-worth divorces involved disputes over cryptocurrency classification. Is it marital property subject to division? Or is it separate property? Without clear legal definitions, judges make up their own rules, leading to unpredictable outcomes for couples.

New Frameworks: MiCA and Beyond

Recognizing that the old binary system is broken, lawmakers are building new categories. The European Union’s Markets in Crypto-Assets (MiCA) regulation, effective June 2024, introduces a third category: "virtual assets." These are distinct from both traditional property and fiat currency. MiCA provides a unified framework for the entire EU, reducing the confusion seen in fragmented national laws.

In the US, the landscape is shifting too. The Uniform Law Commission revised the Uniform Electronic Transactions Act in 2023 to explicitly address cryptocurrency. Meanwhile, the IRS released draft guidance in 2024 proposing a three-tier system:

- Tier 1: Government-issued currency (stablecoins pegged to fiat).

- Tier 2: Non-pegged cryptocurrencies (treated as property).

- Tier 3: Other digital tokens (case-by-case analysis).

Practical Steps for Asset Owners

You don’t need to be a lawyer to navigate this, but you do need to be organized. Here is how to protect yourself regardless of how the law classifies your assets:

- Document Everything: Keep detailed records of acquisition dates, costs, and transaction histories. If crypto is property, these records determine your tax basis.

- Secure Access: Treat private keys like deeds to real estate. Store them securely and include instructions for heirs in your estate plan. Do not rely solely on passwords.

- Consult Specialists: Generalist accountants may not understand the nuance between property and currency classifications. Seek advisors familiar with digital asset taxation, the application of tax laws to cryptocurrencies and blockchain-based assets.

- Monitor Regulatory Changes: The legal landscape is moving fast. What was true in 2023 may change by 2027. Stay updated on local and federal regulations.

The line between property and currency is blurring. As digital assets become more integrated into the global economy, the law will likely continue to evolve, creating new categories that reflect the reality of the digital age. Until then, clarity in your own records is your best defense.

Is Bitcoin considered property or currency by the IRS?

The IRS currently classifies Bitcoin and other cryptocurrencies as property for tax purposes. This means you must report capital gains or losses when you sell, trade, or spend them, similar to stocks or real estate.

How does the EU classify cryptocurrencies under MiCA?

Under the Markets in Crypto-Assets (MiCA) regulation, the EU classifies cryptocurrencies as "virtual assets." This is a distinct category separate from traditional fiat currency and tangible property, providing a specific regulatory framework for issuers and service providers.

What happens to crypto assets in a divorce settlement?

Crypto assets are typically treated as marital property if acquired during the marriage, subject to equitable distribution. However, due to lack of uniform laws, classification can vary by jurisdiction, sometimes leading to disputes over whether it is separate or shared property.

Why is the distinction between property and currency important for taxes?

If an asset is currency, spending it usually doesn't trigger a tax event. If it is property, every exchange (including buying goods with it) is a taxable event requiring calculation of capital gains or losses based on the difference between purchase price and current value.

Can I leave cryptocurrency to my heirs easily?

Leaving crypto to heirs is complex because access relies on private keys rather than institutional accounts. You must include clear instructions in your will or estate plan on how to access the wallets, as executors may not automatically have legal authority to access encrypted digital assets without proper documentation.